Insurance markets have been fundamental to economic expansion throughout history, yet their evolution follows a remarkably consistent pattern: they begin with prohibitively high premiums due to uncertainty, mature through data collection and risk assessment, and eventually enable broader market participation through reduced rates. Understanding this progression is crucial for anticipating how DeFi markets might evolve. After all, insurance markets are fundamentally a function of transferring risk.

Historical Precedents: How Insurance Markets Mature

Maritime Insurance: The story of Lloyd's of London provides perhaps the most illuminating historical parallel. In the 17th century, maritime trade was the backbone of economic growth, but it was plagued by astronomical risks. Ship owners struggled to find capital, and investors were hesitant to back voyages without protection. The solution emerged from an unlikely place: coffee houses.

Edward Lloyd's establishment became a central hub where merchants, sailors, and underwriters gathered to share crucial information. Ships' captains would report on weather patterns they'd encountered. Merchants shared intelligence about the pirate activity. Shipbuilders discussed vessel designs and their seaworthiness. This informal gathering place evolved into something revolutionary: a central clearinghouse for shipping intelligence.

The impact was profound. Underwriters could now differentiate between high and low-risk voyages based on factors like:

- Seasonal weather patterns on specific routes

- The reputation and experience of ship captains

- Ship design and construction quality

- Historical success rates of similar voyages

- Known piracy threats in different regions

As this data accumulated, a fascinating trend emerged: premiums for well-documented routes with experienced captains and quality vessels began to drop significantly. This created a virtuous cycle where ship owners were incentivized to improve their practices and share more information, leading to further premium reductions.

Fire Insurance: The Great Fire of London in 1666 sparked another crucial development in insurance markets. Initial fire insurance premiums were exorbitant as insurers had no systematic way to assess building risks. However, the Nicholas Barbon Insurance Office and others began methodically collecting data about:

- Building materials and construction methods

- Proximity to other structures

- Fire prevention measures

- Historical fire incident patterns

- Emergency response capabilities

This data collection revolutionized the industry. Insurers could now offer lower premiums for buildings that incorporated fire-resistant materials or maintained certain safety standards. This created economic incentives for better construction practices, leading to a broader transformation in urban development.

Auto Insurance: The automotive insurance industry's development in the 20th century provides a more recent example of this pattern. Early car insurance was prohibitively expensive due to limited data about accident risks. As insurers accumulated information about:

- Driver demographics and behavior patterns

- Vehicle safety features and performance

- Road conditions and traffic patterns

- Accident frequency and severity

- Repair costs and liability trends

They developed increasingly sophisticated risk models. This evolution continues today with telematics and usage-based insurance, where real-time data collection enables even more precise risk assessment and pricing.

The DeFi Challenge: New Risks, Time-Tested Solutions

Currently, the DeFi space faces challenges remarkably similar to these historical examples. Institutional investors see the potential for significant returns but lack the risk management tools they're accustomed to in traditional finance. The hesitation of major allocators isn't primarily about the presence of risk—after all, traditional finance carries significant risks as well. The crucial difference is that TradFi risks can be quantified, priced, and hedged. This is in large point because it isn’t immutable: it's a coordination system that can be edited if there is a mistake. Not the case with crypto which means we have to get it right the first time, every time.

To make DeFi the new financial rails of the world, this insurance problem needs fixing so that insurance companies can run successfully providing the proper risk mitigation to those that would otherwise not allocate funds to DeFi. At its core, the fundamental issue is that of data.

The challenges in DeFi are multifaceted:

Smart Contract Risk Unlike traditional financial instruments, smart contracts introduce new categories of technical risk that are difficult to quantify. Traditional actuarial models don't account for:

- Code vulnerabilities

- Oracle failures

- Governance attacks

- Protocol interaction risks

Additionally, all of this data is NOT centralized or accessible in a simple way. To even begin to start underwriting technical risk we need a way of proving all the data relating to the above and more. Not only that, but we need to be able to prove that major code vulnerabilities are protected. In the same way that shipping underwriters began to lower premiums on routes they could trust, DeFi underwriters will lower premiums on smart contracts that can prove that they have the proper security guarantees in place, and we don’t just mean audits.

These factors create a familiar scenario: without reliable insurance markets, many institutions maintain minimal crypto exposure or avoid the space entirely.

The Solution

Here is how Phylax is going to single-handedly fix this drought of data that is prohibiting insurance markets from flourishing.

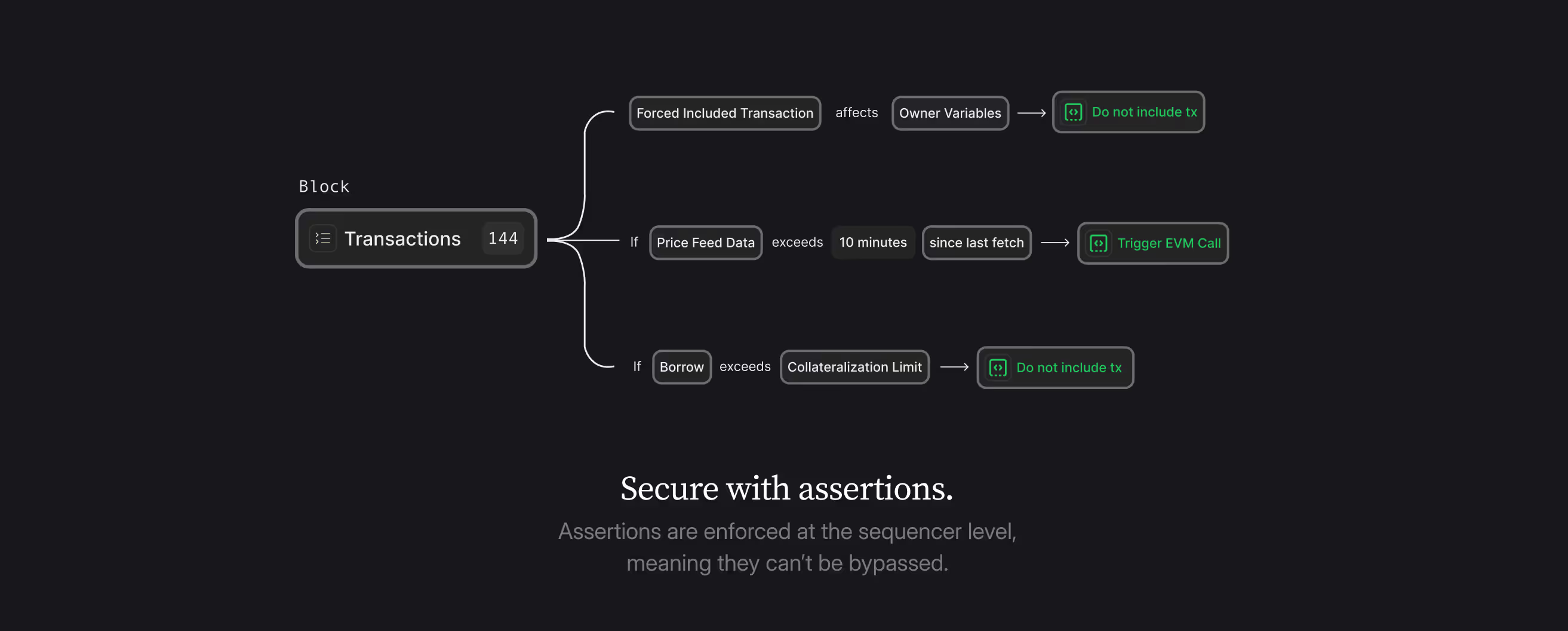

We are going to enable dApps to define security rules (we refer to them as assertions) that the block builder itself enforces. These rules can govern oracle price fluctuations, fundamental invariants, cRatios on lending positions, share/asset value equilibriums, or anything else. The block builder runs the PhEVM, our simulation engine that checks the pre-state of each contract that an assertion is associated with against the state that the assertion defined as a hack to ensure that the assertion is never invalidated. Read more about the PhEVM and how it works here.

Now here’s the kicker: in addition to stopping hacks we are going to let everyone prove all assertions of any protocol. What’s more, they will also be able to see all previous hacks that were prevented and all the vulnerabilities that were found. In simple terms, everyone will have a full picture of any given dApp’s security history.

Something to consider is that common patterns to contracts, such as certain ERCs or use-case-specific contracts (e.g., lending, swaps, NFTs) mean common smart contract patterns and therefore the hacked state of each protocol too. Through seeing prevented hacks and watching as dApps institute the same assertions to protect their own users we will collect all the data necessary to find what parts of a contract are targeted and what assertions prevent that part from being exploited. And remember, it's the network itself (Base, Mantle, Ink, etc) doing the prevention. This is exactly the sort of process that will enable underwriters to start bringing down costs, specifically for the protocols that use common contract patterns and implement time-tested assertions.

And because security is critical to insurance and the success of our industry broadly we decided a long time ago that we need to be completely open source. That means every single assertion ever written can be copied by another dApp and implemented immediately. Crypto "winning" is not as simple as securing one protocol that people can then trust: we have to restore our industry's image and that means making every protocol safe.

Just as Lloyd's Coffee House transformed maritime trade by centralizing risk data, we're creating the foundation for DeFi's future as the backbone of finance from institutions down to your grandma. Every assertion written and shared, every hack prevented and documented, builds toward a future where capital can flow as confidently through DeFi as it does through traditional markets. The revolution in risk assessment starts with transparency - and it starts with us.

Contact us here to leverage the Credible Layer or build with us.

.png)

.png)